The article contains data provided by Saxobank, Reuters, ICCO, HCCO, Rabobank

1. Season 2024/2025

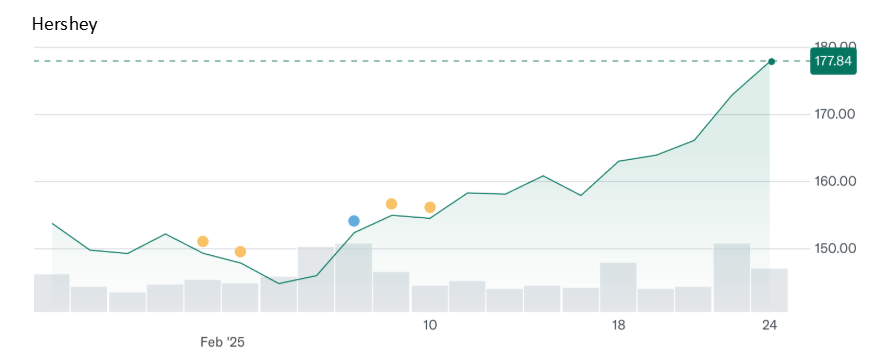

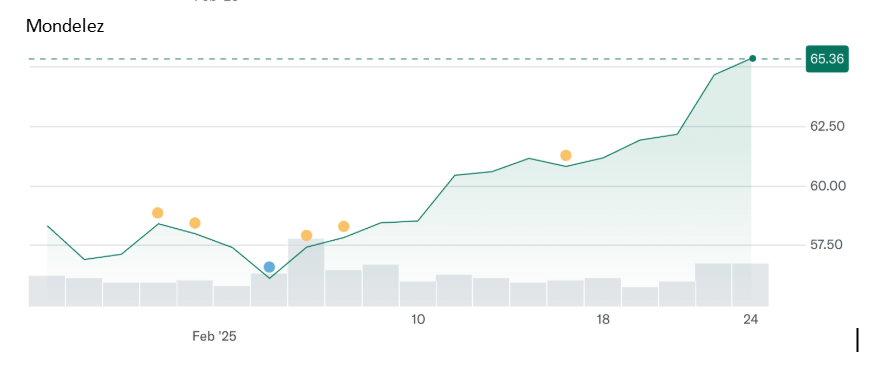

The sales of leading global cocoa industry companies are showing decent results.

For instance, Hershey reported a sales increase in the fourth quarter, and the stocks of Hershey, Mondelez, and Barry Callebaut are on the rise.

The cocoa harvest season in Côte d’Ivoire continues, and we have encouraging data on cocoa bean arrivals at ports. As of February 24, a total of 1,368,000.00 tons have been delivered to ports. Based on this data, we are ahead of the previous harvest year by 17% compared to last season (although, at the start of the harvest, we were ahead by nearly 40%). However, there is a clear trend of declining arrivals. Over the past 10 weeks, significantly less beans have been delivered to ports compared to a year earlier.

The main harvest will be better than last year, but not good enough, and we are very likely to see a fourth consecutive year of supply deficit.

However, up to 200,000.00 tons have been illegally exported to Guinea, flooding the market and being sold at a discount compared to exchange prices.

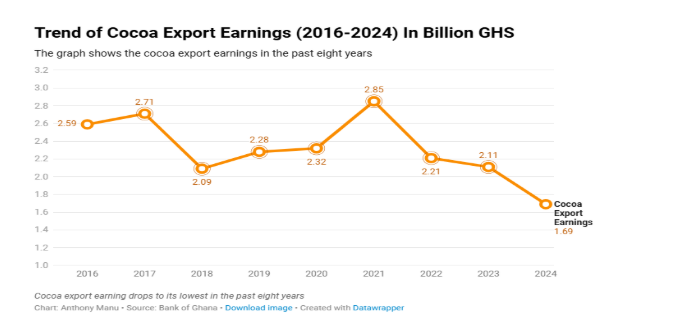

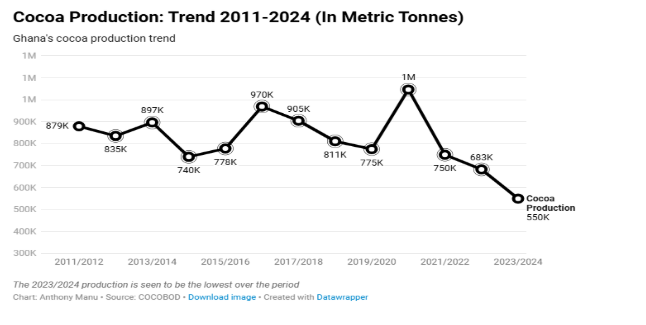

Below are two tables showing the earnings of the Ghana Cocoa Board and cocoa bean production in Ghana. A crisis in the industry is evident, as we have previously reported several times, which is also one of the reasons for high prices over the past two years. Demand significantly exceeds supply.

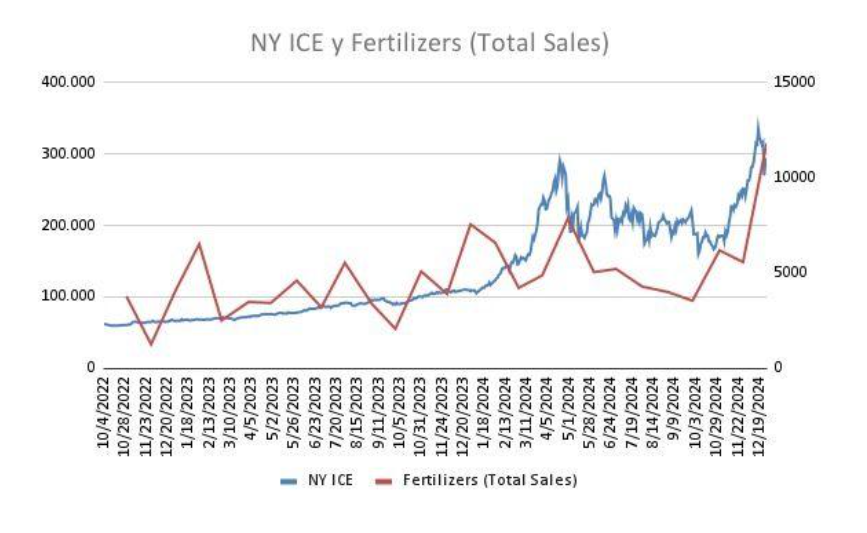

On the other hand, Ecuador is currently experiencing a real boom in fertilizer sales for cocoa plantations. This suggests that the country is likely to have a very good harvest in the 2025/2026 season.

This trend is already reflected in the very strong figures for the 2024/2025 season.

The market continues to experience a physical shortage of cocoa beans.

Certified stock in U.S. warehouses declined in January, reaching its lowest level in at least the past 10 years. As of February 24, the number of bags stands at approximately 1,400,000,00 which is around 90,000.00 tons — a clear increase from 80,000.00 tons a month earlier, but still significantly insufficient.

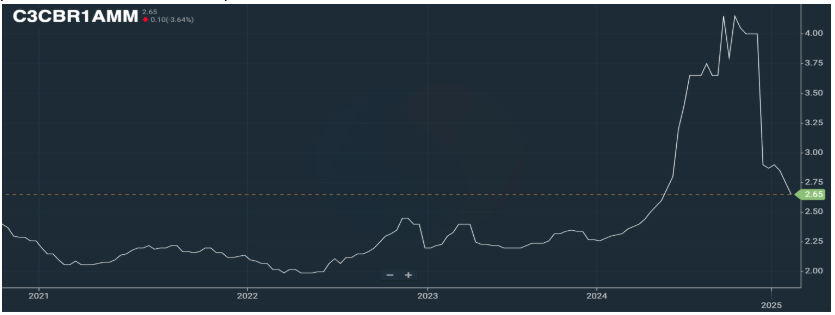

The ratio for cocoa butter is currently at 2.65, marking a significant correction from the peak levels of over 4 ratio points during the summer of 2024. The actual price remains stable, with a slight decline possible over the next two quarters.

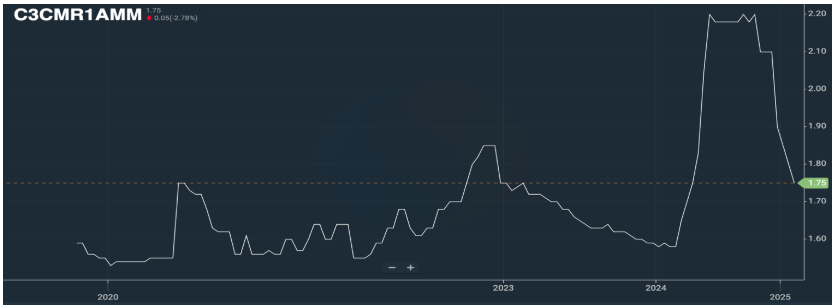

The ratio for cocoa liquor stands at 1.75, showing a slight downward correction trend throughout 2025.

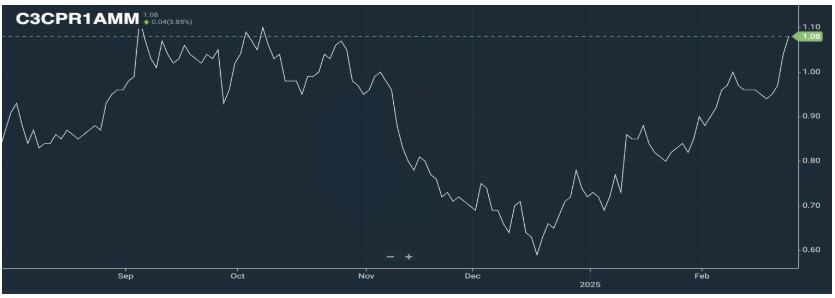

The ratio for cocoa powder is at 1.08, significantly higher than the previous month, leading to an increase in the final product price compared to last month.

As of today, the exchange price in euros is €9,000.00 per ton.

FOB West Africa ratios for December 2024 deliveries are at the following levels:

Cocoa Liquor

1.75, with a steadily declining trend toward 1.7 by 2nd quarter of 2025. At the current exchange price, the Q1 price will be around €19,000.00 per ton.

Natural Cocoa Butter

2.65, with a declining trend over the next four quarters to 2.5. At the current exchange levels, the price in the first/second quarter will be around €28,500.00 per ton.

Cocoa Powder

The ratio for cocoa powder has remained nearly unchanged from last month, staying at 1.08 relative to the exchange price.

Natural cocoa powder price starting from €9,500.00 per ton

Alkalized cocoa powder price starting from €9,750.00 per ton

2. Technical Analysis

The New York market has shown a long-awaited correction, completing the second wave correction lower than previously expected. Most likely, we will move upward from these levels, and the previous forecast of $14,000.00 per ton and higher remains valid.

It is likely that by the end of February, we reached the bottom of the correction in the short term. Currently, we are in a new growth phase, finishing the corrective movement of wave 2, followed by an upward price movement forming wave 3—the longest and fastest wave.

Our advice to clients remains the same: buy any price correction, as it may be short-lived. With the current market volatility, we could observe price swings of over $1,000.00 per day.

Weather

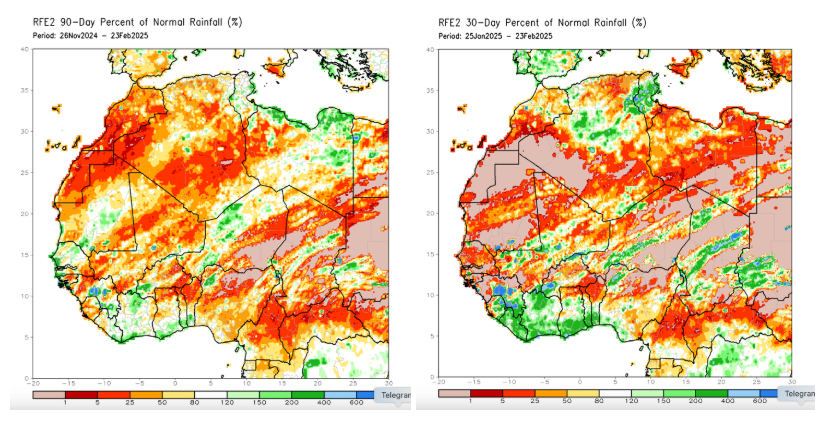

Rainfall levels in West Africa over the past 30 and 90 days have been above normal. In the last month, we have seen heavy rains, which should contribute to strong harvest figures in late July/August and likely lay a good basis for the next main harvest.